Although only a small segment of the American population, sovereign citizens have managed to cause significant headaches for commercial lenders over the past several decades. While their primary antagonists are typically government agencies, sovereign citizens have developed a host of pseudo‑legal theories and tactics aimed squarely at avoiding private debts and obstructing creditors. This article provides lenders with a clear overview of core sovereign citizen beliefs and highlights common documentary indicators that a prospective or current borrower may subscribe to this ideology.

Who Are Sovereign Citizens?

“Sovereign citizen” is a broad and imprecise label encompassing an ideologically diverse range of individuals and groups who share one foundational belief: that the United States government, as presently constituted, is illegitimate and lacks authority over them.1

The most commonly held sovereign citizen beliefs rest on a distorted understanding of American history centered around two dates: 1868 and 1933.

In 1868, adherents believed that the passage of the Fourteenth Amendment created two classes of citizens: (1) “de jure” citizens governed only by what they call “common law,” and (2) “federal commercial citizens,” who are allegedly subject to illegitimate federal authority.2 Sovereign citizens believe, by some artifice or another, that they are or have become de jure citizens and thus are exempt from statutes and regulations, and the Uniform Commercial Code (UCC).3

Second, in 1933, sovereign citizens contend that the United States declared bankruptcy when it abandoned the gold standard.4 In their understanding, in place of the gold standard, the federal government created separate “strawman” identities for every American at birth linked to secret United States Treasury accounts, which contain vast sums of money — sums of money that the government now uses as collateral.5 The strawman identity, they claim, is signaled by the appearance of the person’s name in ALL CAPITAL LETTERS on government documents and financial instruments.6 Through use of the correct pseudo-legal language or document rituals, sovereign citizens believe that: (1) they can access the funds in these imaginary strawman accounts and (2) any debt, contract or legal obligation only binds their strawman identity, not their real “flesh-and-blood” self.7

While adherents come from all walks of life, this ideology particularly attracts individuals experiencing severe financial distress or extreme frustration with government or banking institutions.

For lenders, the practical risk is immediate: Sovereign citizens can increase servicing costs, create friction in default proceedings, disrupt collections and occasionally pose safety concerns for frontline staff. Recognizing early indicators can significantly reduce these risks.

How Sovereign Citizens Try to Avoid Private Debt Collection

Sovereign citizens employ a variety of schemes to frustrate the enforcement of valid loan obligations. Two of the most common involve: (1) challenging the validity of the original loan agreement because it binds only the strawman and not the “flesh-and-blood” person; and (2) attempting to discharge debt through pseudo-legal inscriptions, often referred to as “Accepted for Value” (A4V) schemes.

Denying the Contract’s Validity

A frequently used tactic is asserting that the borrower signed the agreement only as an agent for their strawman identity and therefore did not personally consent to the contract.8 Under this theory, only the fictional entity is bound by the loan. Some also argue that because all contracts are governed by the UCC, and because they are “de jure” citizens, all contracts are unenforceable against them.9

“Accepted for Value” (A4V) Schemes

In A4V schemes, sovereign citizens attempt to “pay” debts using specific inscriptions, stamps or phrases that they believe activate their strawman’s Treasury account or serve as alternative contractual consideration.10 The most recognizable is “Accepted for Value,” but sovereign citizens deploy a wide range of pseudo‑legal phrases. When used, adherents believe that a binding contract is automatically created upon the lender’s receipt of the inscribed documents.11

Depending on their interpretation, sovereign citizens believe that this scheme results in one of two outcomes.

First, adherents may believe that the inscribed document forces the lender to satisfy the debt by withdrawing funds from their strawman’s secret Treasury account.12 Alternatively, adherents believe that if these phrases are used in conjunction with postage stamps affixed to the document, the stamp itself becomes an adequate substitute consideration that satisfies the debt upon receipt.13

Neither of these schemes has any legal validity. Regardless, lenders should learn to recognize the indicators signifying when sovereign citizens are attempting to employ them so that the issue can be promptly escalated to legal counsel.

Sovereign Citizen Indicators: What Lenders Should Watch For

The good news is that sovereign citizens tend to announce themselves through distinctive markings, formats or inscriptions on documents. The following indicators are among (but not all of) the most common.

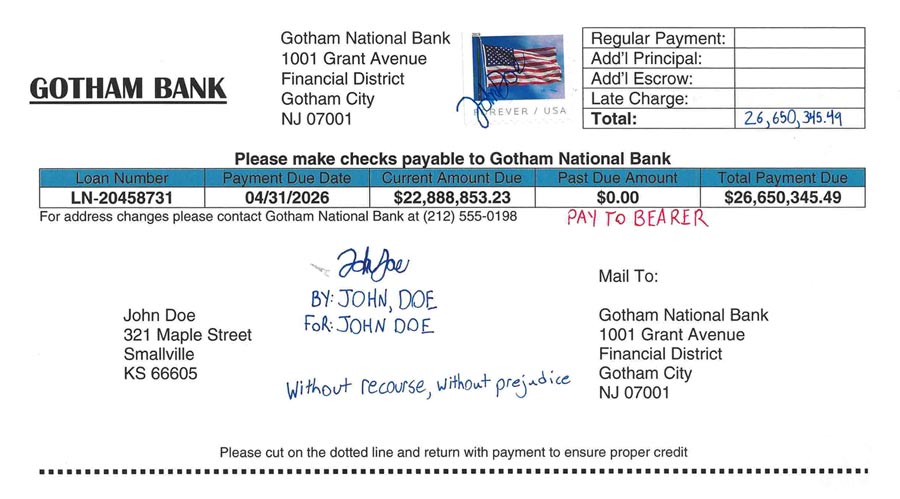

Postage Stamps Affixed to Documents

Affixing postage stamps to loan documents is one of the clearest red flags. Sovereign citizens (incorrectly) believe that affixing these stamps transforms their documents into protected “correspondence” and thus prevents any United States government from exercising jurisdiction over them.14 Additionally (or alternatively), adherents contend that the postage stamp itself constitutes binding consideration in lieu of repayment of the underlying loan.15 Regardless of the specific rationale, mainstream borrowers do not engage in this behavior; its presence should be treated as a significant warning sign that the borrower is a sovereign citizen.

ALL CAPS or Unconventional Name Formatting

Another common indicator is when the borrower signs their name in all capital letters (JOHN DOE), formatted with unusual punctuation (Doe;. John) or both (DOE;. JOHN).16 By signing the document in this manner, sovereign citizens believe that they have properly differentiated their “flesh-and-blood” selves from their strawman identity and that any signature they provide is as an agent for the strawman.17 Accordingly, to them, any agreement signed in such a manner is not binding upon their flesh-and-blood self.18

Although such formatting occasionally results from a confused but well-meaning borrower, these signatures should prompt heightened awareness from lenders, as they may indicate the borrower’s subscription to the sovereign citizen ideology.

“Without Recourse” and “Without Prejudice” Language

Perhaps the most widely used documentary marker is the addition of “Without Prejudice” and “Without Recourse” near or within the signature block. They believe these statements create a record that the sovereign signed under protest, did not consent to the court’s or lender’s authority, and cannot be held personally liable.19 While sovereign citizens draw these statements directly from UCC §1-308, they distort their meaning far beyond any legitimate interpretations, like magic talismans that protect those who invoke the phrases from any government jurisdiction.20

The presence of these phrases near a signature block should be treated as a strong indicator of sovereign citizen ideology.

This is an anonymized recreation of a loan document Baird Holm LLP received, which depicts some of the symbols sovereign citizens use to attempt to avoid paying debts. Using this article as a reference, see how many red flags you can identify.

Conclusion

Although courts have uniformly rejected every sovereign citizen theory and scheme just described, these tactics remain disruptive and costly for lenders. Early identification is the most effective way for lending institutions to limit the expenses and threats created by sovereign citizens. By training frontline employees to recognize the indicators outlined in this article and to escalate promptly to legal counsel, lenders can better manage the risks posed by this small but ever-present menace at the fringes of American society.

- A Quick Guide to Sovereign Citizens 1, UNC Sch. of Gov’t (rev. Nov. 2013), https://www.sog.unc.edu/sites/www.sog.unc.edu/files/Sov%20citizens%20quick%20guide%20Nov%2013.pdf.

- Id. at 1–2.

- J.M. Berger, Without Prejudice: What Sovereign Citizens Believe 4–5, G.W.U. Program on Extremism (June 2016), https://extremism.gwu.edu/sites/g/files/zaxdzs5746/files/downloads/JMB%20Sovereign%20Citizens.pdf.

- FBI Domestic Terrorism Operations Unit II, Sovereign Citizens: An Introduction for Law Enforcement 6–7 (Nov. 2010) (unclassified/law enforcement sensitive).

- Id.

- Id.

- Mellie Ligon, The Sovereign Citizen Movement: A Comparative Analysis with Similar Foreign Movements and Takeaways for the United States Judicial System, 35 Emory Int’l L. Rev. 297, 301–2 (2021).

- Berger, supra note 3, at 5–6.

- Id.

- Anti-Defamation League, The Sovereign Citizen Movement: Common Documentary Identifiers & Examples 9–10 (2016).

- Id.

- FBI Domestic Terrorism Operations Unit II, supra note 4, at 6–7.

- Donald J. Netolitzky, Organized Pseudolegal Commercial Arguments as Magic and Ceremony, 55 Alberta L. Rev. 1045, 1063–64 (2018).

- Id. at 1058–59.

- Id. at 1063–64.

- Anti-Defamation League, supra note 10, at 2, 5.

- Id.

- Id.

- Berger, supra note 3, at 5.

- Anti-Defamation League, supra note 10, at 3.