Chris W. Bell, Associate General Counsel at Compliance Alliance

The COVID-19 pandemic has changed American life as we know it. As the country continues to deal with the health crisis, the effects of containment measures ripple through the American economy. Unemployment remains high as state economies expand and contract in inverse proportion to the virus’s spread. Regulators are in an arms race with rapidly changing markets, forcing banks to adapt to an ever-changing regulatory landscape. Even as we struggle to deal with the immediate concerns, we know the effects of this pandemic will be with us for some time. Economic shocks will continue to reverberate and play out in the housing markets around the country. As we shift into the next phase of operating in the pandemic and consider what options exist to help struggling mortgage borrowers, we should take note of the status of the expansive mortgagor protections passed by Congress, federal agencies, and other government authorities.

Protection for Federally Backed Mortgage Loans

In the early days of the pandemic, Congress passed the Coronavirus Aid, Relief, and Economic Security (“CARES”) Act. One of the primary sections of this law established a 60-day moratorium on foreclosure proceedings against homeowners with federally-backed mortgage loans. The CARES Act’s mortgage foreclosure moratorium applied to single-family residential mortgage loans secured, guaranteed, or made by FHA, USDA, VA, or Fannie Mae or Freddie Mac. Originally scheduled to expire at the end of June, the various agencies extended the moratorium on foreclosures and evictions until at least August 31, 2020.

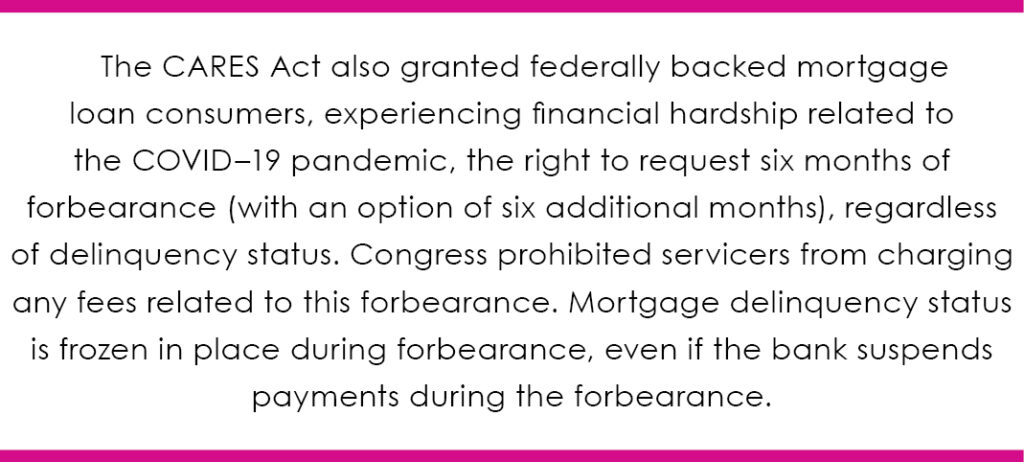

The CARES Act also granted federally backed mortgage loan consumers, experiencing financial hardship related to the COVID–19 pandemic, the right to request six months of forbearance (with an option of six additional months), regardless of delinquency status. Congress prohibited servicers from charging any fees related to this forbearance. Mortgage delinquency status is frozen in place during forbearance, even if the bank suspends payments during the forbearance. As it stands today, customers can request forbearance under the CARES Act until the earlier of the end of 2020, or the end-date of the national emergency concerning the novel coronavirus disease outbreak declared by the president on March 13, 2020, under the National Emergencies Act.

State and Local-level Protection

Many state and local authorities enacted policies to protect mortgage borrowers and renters. The details of these state and local foreclosure bans vary. Banks should refer to the official websites for their state and local governments to assess the scope and requirements of applicable prohibitions. While effective dates vary widely, many of these protections remain in effect until respective governors lift statewide emergency declarations.

Private loans

The CARES Act provided no relief for loans that are not federally-backed. Banks should refer to the appropriate investor guidelines for mortgages sold to private investors. Banks should refer to guidance from its regulators concerning their expectations regarding non-federally-back mortgage loans held in portfolio.

Troubled Debt Restructuring (“TDR”)

If neither a federal nor state moratorium applies to a residential mortgage you hold in portfolio, you may still be able to exercise your authority to assist pandemic-effected borrowers who are struggling financially. Regulators have urged banks to work with customers and prudently modify loans in a safe and sound manner. Section 4310 of the CARES Act provided banks relief from TDR. In April, regulatory agencies issued revised interagency guidance to help banks sort modification requests into three groups: (1) loan modifications covered by Section 4310 of the CARES Act; (2) those outside of Section 4310 deemed not to be TDRs; and (3) those outside of Section 4310 that may be TDRs. In June, regulators released new interagency safety and soundness examiner guidelines. These guidelines instruct examiners to not criticize institutions for doing so as part of a risk mitigation strategy intended to improve existing loans, even if a restructured loan ultimately results in adverse credit classifications.

To be covered by Section 4310 of the CARES Act, a loan modification must: (1) relate to COVID-19, (2) be executed between March 1st and December 31st (assuming the current national emergency does not end earlier than the end of the year), and (3) the underlying obligation must be not more than 30 days past due. If a loan modification meets these three criteria, financial institutions do not have to report it as a TDR; however, the financial institution should maintain records of the volume of such loan modifications.

If a loan modification fails to meet any of the three criteria for Section 4310 coverage, it does not automatically result in a TDR. Regulators will deem a modification as not to constitute a TDR if it relates to COVID-19, extends no more than six months, and the underlying obligation is not more than 30 days past due. The only subjective criterion is the relationship of the modification to COVID-19. As a best practice, banks should have the borrower certify that the requested change is due to COVID-19. To not raise HIPAA concerns, the certification should be general and not address specific health details. While such a certification is not required to be in the loan file, it would show future examiners that the lender followed the guidance in good faith. If a bank receives a modification request that is outside the scope of Section 4310 and does not meet the described criteria, the bank should assess whether the modification would be a concession to the borrower that the bank would not otherwise consider and act accordingly.

As with everything related to the COVID-19 pandemic, expect mortgage foreclosure protections to change as the country continues to deal with the long-term effects of our national crisis. The federal agencies may extend the protections relating to the loans they back, and Congress will undoubtedly reassess the CARES Act’s protections as the end of its covered period draws near. Despite how things change, you can count on the Texas Bankers Association to bring you the most up-to-date information available as we walk hand-in-hand through this crisis.

Chris W. Bell is an associate general counsel at Compliance Alliance. He has worked in the legal department of a federal savings bank and for the Texas Department of Banking. He is one of the C/A hotline advisors.